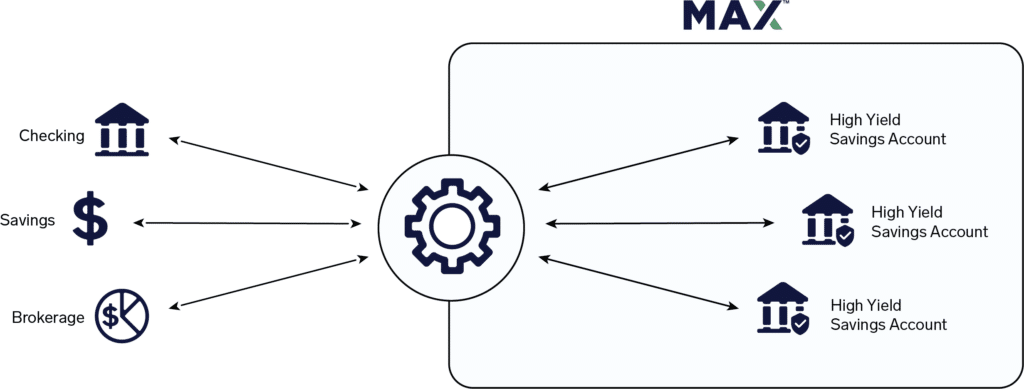

How does Max work?

Max helps you allocate your cash across a network of trusted online banks offering market-leading interest rates, maximizing your interest earnings and FDIC insurance coverage.

By helping you spread your cash across multiple high-yield savings accounts, Max helps ensure market-leading returns and increased FDIC insurance coverage.

Max’s patented service monitors changing interest rates daily. Each month, Max helps you allocate your cash based on the parameters you set. Max then passes along your transfer instructions to your banks so that they can optimally allocate your funds among your own accounts. We call this an “Optimization.”

During each optimization, your cash will flow between your high-yield savings accounts via a central checking account. This checking account links your accounts together so you can keep your existing bank relationships and track transfers through a central account.

You are always in full control of when and how you allocate your funds among your own bank accounts, and you can change system settings at any time. You also retain full control over each account individually, so while Max provides a single dashboard where you can see all of your accounts and request funds transfers, you can also move, deposit, or withdraw your money directly with your banks as needed.

How does Max work?

Max helps you allocate your cash across a network of trusted online banks offering market-leading interest rates, maximizing your interest earnings and FDIC insurance coverage.

By helping you spread your cash across multiple high-yield savings accounts, Max helps ensure market-leading returns and increased FDIC insurance coverage.

Max’s patented service monitors changing interest rates daily. Each month, Max helps you allocate your cash based on the parameters you set. Max then passes along your transfer instructions to your banks so that they can optimally allocate your funds among your own accounts. We call this an “Optimization.”

During each optimization, your cash will flow between your high-yield savings accounts via a central checking account. This checking account links your accounts together so you can keep your existing bank relationships and track transfers through a central account.

You are always in full control of when and how you allocate your funds among your own bank accounts, and you can change system settings at any time. You also retain full control over each account individually, so while Max provides a single dashboard where you can see all of your accounts and request funds transfers, you can also move, deposit, or withdraw your money directly with your banks as needed.

How do Optimizations work?

During an optimization, Max will help you allocate your cash optimally to help you earn more.

Once a month, Max will help you optimize your accounts according to your settings. You can pause, suspend, or change the date of your monthly optimization, and you can initiate an “on-demand” optimization from your Max Dashboard whenever you like.

During an optimization, Max will calculate a set of transfers to help you move your funds to your highest-yielding savings accounts. Once your highest-yielding account is full up to the FDIC insurance limit, your remaining funds will go to your next-highest-yielding bank account, and so on, until all your funds have been allocated across your bank accounts. This enables you to earn the highest returns while also keeping your funds fully insured. All funds transfers flow through your central checking account so you can track your transfers through one account. With Max, your funds transfers are handled by your own banks and typically take 1-2 business days. Some transfers are even completed same-day.

Max does not have the authority to open new bank accounts without your authorization, so funds will only flow between the accounts that you have opened. Max makes it easy to open multiple accounts at once using the patented Max Common Application. The more accounts you open, the more flexibility Max will have to help you earn the highest yields.

How does Max work?

Max helps clients allocate their cash across a network of trusted online banks offering market-leading interest rates, maximizing their interest earnings and FDIC insurance coverage.

By helping clients spread cash across multiple high-yield savings accounts, Max helps ensure market-leading returns and increased FDIC insurance coverage.

Max’s patented service monitors changing interest rates daily. Each month, Max calculates an optimal allocation of your clients’ cash based on the parameters they set. Max then passes along their transfer instructions to their banks to optimally allocate their funds across their own accounts. We call this an “Optimization.”

During each optimization, your clients’ cash will flow between their high-yield savings accounts via a central checking account. This checking account links your clients’ accounts together so they can keep their existing bank relationships and track transfers through one account.

Max members are always in full control of how and when funds are allocated, and they can change their system settings at any time. Clients also retain full control over each account individually, so while Max provides a single dashboard where they can see all of their accounts and request funds transfers, they can also move, deposit, or withdraw their money directly with their banks as needed.

How do Optimizations work?

During an optimization, Max will help your clients allocate their cash optimally to help them earn more.

Once a month, Max will help your clients optimize their accounts according to their settings. They can pause, suspend, or change the date of their monthly optimization and can also initiate an “on-demand” optimization from the Max Dashboard whenever they like.

During an optimization, Max will calculate a set of transfers to help your clients allocate their funds to their highest-yielding savings accounts. Once the highest-yielding account is full up to the FDIC insurance limit, the remaining funds will go to the next-highest-yielding bank account, and so on, until all funds are allocated across their bank accounts. This enables your clients to earn the highest returns while keeping their funds fully insured. All funds transfers flow through their central checking account. Transfers are handled by your clients’ own banks and typically take 1-2 business days to be completed, although some transfers occur same-day.

Max does not have the authority to open new bank accounts without your clients’ authorization, so funds will only flow between the accounts they have opened. Max makes it easy to open multiple accounts at once using the patented Max Common Application. The more accounts opened, the more flexibility Max will have to help your clients earn the highest yields.